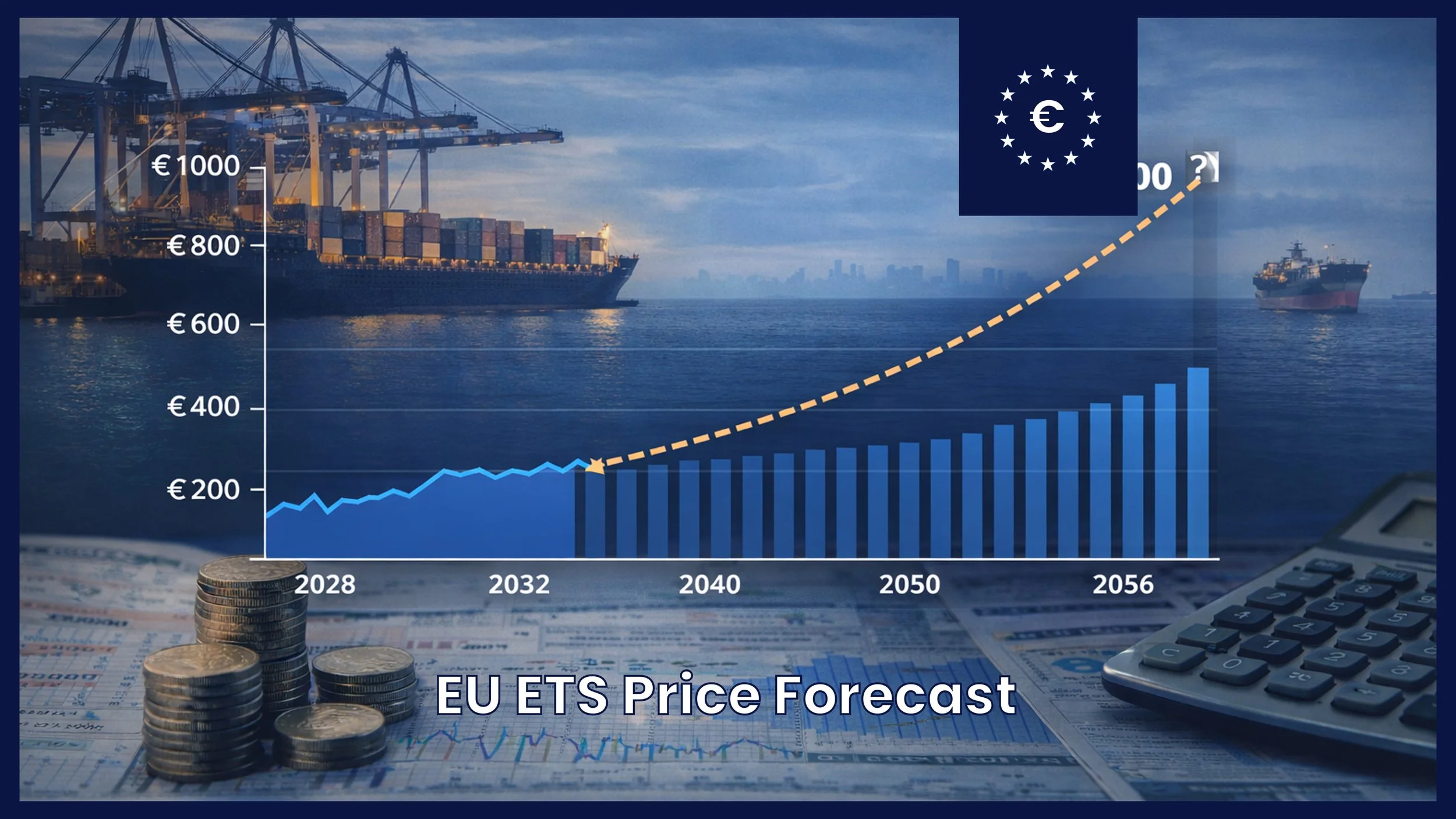

EU ETS Price Forecast - 2026

EUA price is expected to rise by ~7% per year, potentially reaching €500 in 2045 as supply tightens

The EU Emissions Trading System (EU ETS) is rapidly becoming one of the most important cost drivers for shipping. As maritime transport is phased into the system and the total number of available European Union Allowances (EUA) decreases, carbon prices are expected to rise steadily in the coming decades.

Based on current projections and supply reductions under the EU ETS framework, allowance prices may increase by roughly 7% annually, potentially reaching €400–€500 per tonne of CO₂ by the 2040s. This increase is driven primarily by the declining supply of allowances, stricter climate targets, and growing demand from multiple sectors competing for the same carbon budget.

Why EUA price is expected to rise

The key mechanism behind EU ETS price increases is the gradual reduction of available emission allowances. Each year the total number of allowances issued by the EU declines through the Linear Reduction Factor (LRF). This mechanism steadily tightens the overall carbon budget for all participating sectors. At the same time, the EU is strengthening its climate ambitions under the Fit for 55 framework and beyond. As emissions caps become more restrictive, companies must either reduce emissions or purchase allowances from a shrinking pool.

Shipping entered the EU ETS in 2024, adding another large sector to the system. Over time, more emissions will be covered while the overall allowance supply continues to fall. In other words:

Price rise because more demand, fewer allowances.

This structural supply squeeze is the primary reason many forecasts expect long-term carbon prices to rise significantly. Most forecasts suggest carbon prices rising gradually toward the €400–€500 range over the coming decades. Personally, I would not be surprised if prices temporarily exceed €1,000 per tonne in certain periods. The reason is simple: EU ETS markets historically experience strong price swings when supply tightens faster than expected. If emission reductions lag behind policy targets or if multiple sectors compete aggressively for the same allowances, temporary shortages could push prices much higher than long-term averages.

In other words, the long-term trend may be steady, but the path toward it could be volatile.

-

This analysis is part of the Sustainable Ships Fuel Properties & Cost Guide, where we compare marine fuels based on:

Energy density

Storage requirements

Retrofit complexity

CAPEX and OPEX impacts

Regulatory compliance considerations

If you're working on fuel selection, newbuild design, or retrofit strategy, the guide may be useful.

Sign up for premium tools and benefits

The Fuel Properties and Cost Guide is a technical reference and strategic planning tool for evaluating marine fuels under today’s evolving regulatory landscape. Aligned with FuelEU Maritime, EU ETS, and the IMO Net-Zero Strategy, it benchmarks 22 fuels from HFO and MGO to e-methanol and bio-LNG on properties such as LCV, GHG intensity, flash point, CH₄/N₂O emissions, and VLSFO-equivalent cost.

Use Credit card, Stripe, PayPal or Apple Pay (only on iPhone). Contact the helpdesk for payment by invoice.

Don’t want to sign up? Check pay-per-use options

References

Sustainable Ships - EU ETS

You might also like

This case study compares three compliance strategies for FuelEU (paying the penalty (business as usual), buying pool credits from a third party, and blending biofuels) for a representative 4-ship fleet over 2026–2040. Results show that pooling and biofuels both beat business as usual by 6–7%, but it is a coin toss on which is better for you. The outcome is highly sensitive to B100 price and tightens structurally in favour of biofuels after 2030, making this a tipping-point question rather than a one-off choice.