ETD

Energy Taxation Directive

The ETD is the principal taxing scheme used for fossil and low-carbon fuels in EU

About ETD

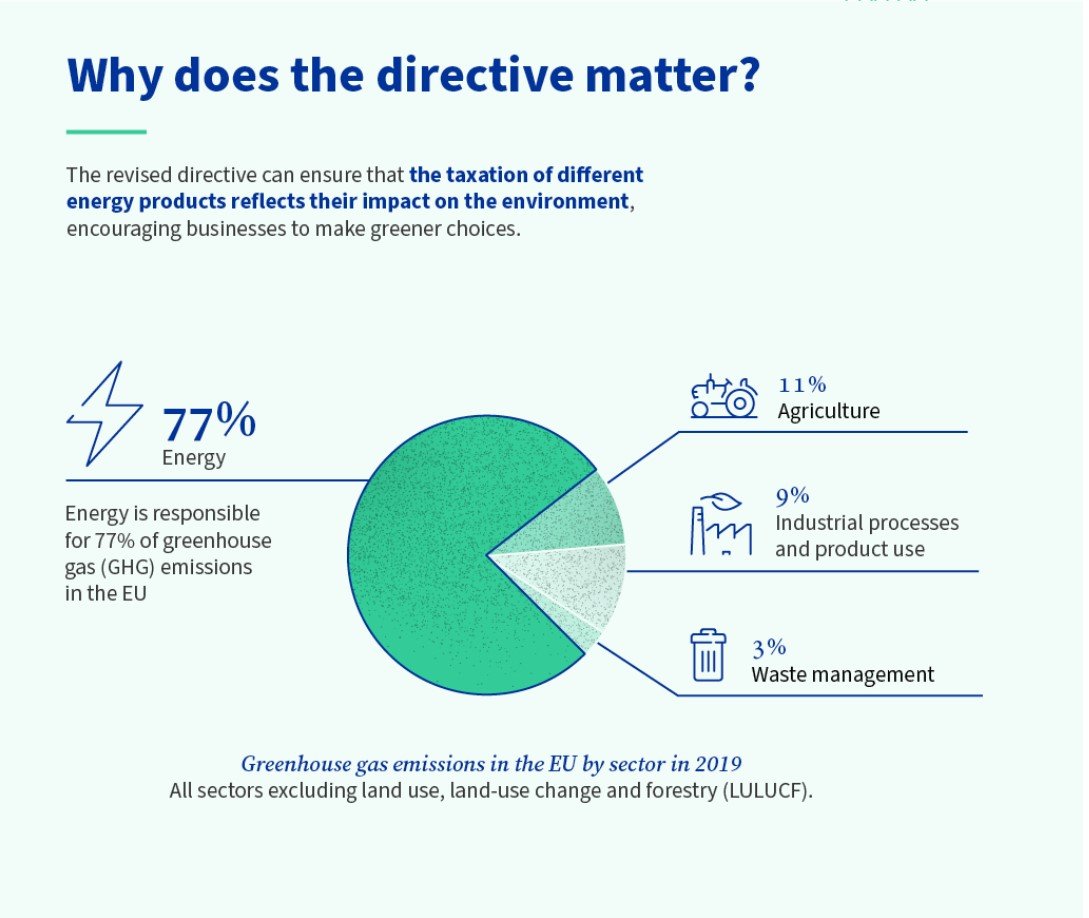

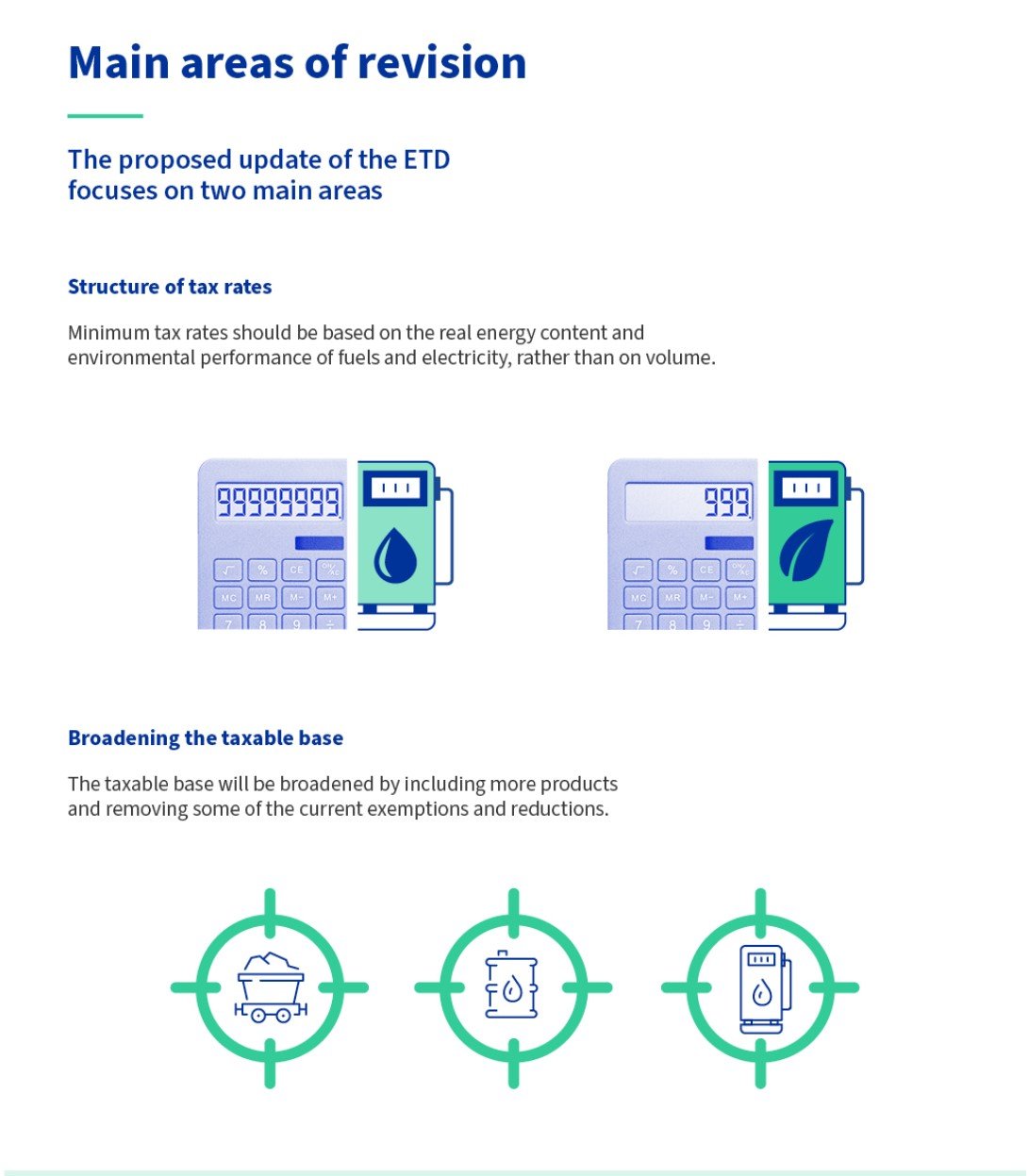

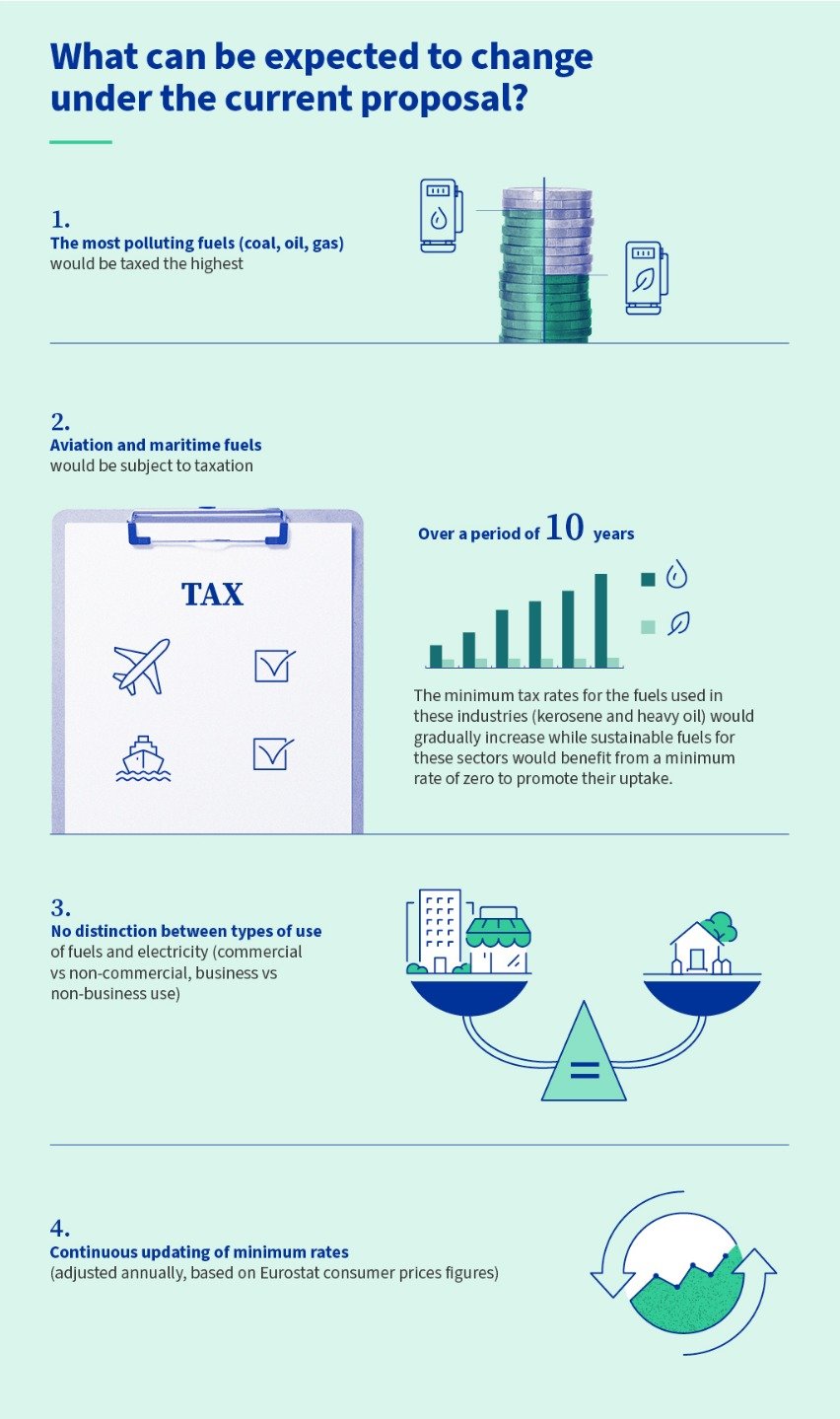

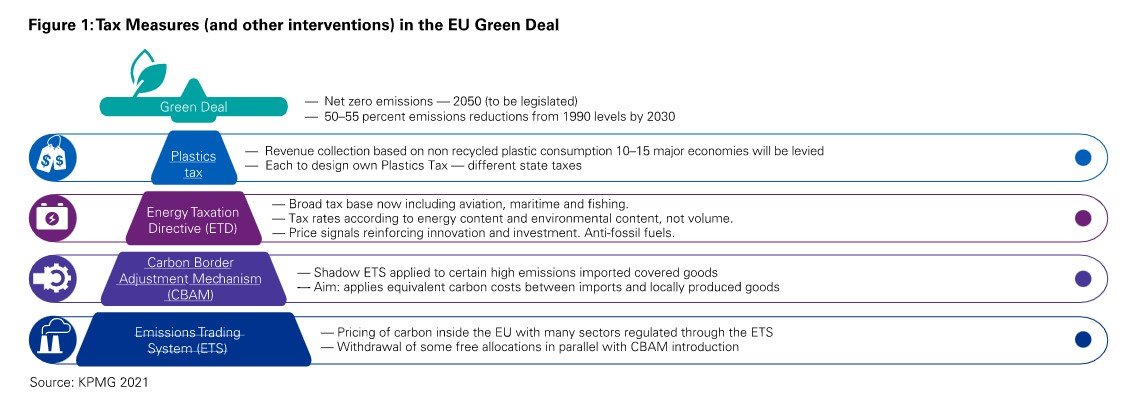

The EU’s fit for 55-package proposes a revision of the Energy Taxation Directive (ETD), which was adopted in 2003. The ETD would be updated to align with current EU climate and energy objectives, incentivize investment in clean technologies, no longer favor fossil fuels, and improve clarity and legal certainty for member states. The ETD currently employs a taxation mechanism that allows subsidies in favor of fossil fuels. Under the new revision, the fuels that pollute most will be taxed at higher rates.

For the shipping industry, energy products and electricity produced from fossil fuels used in waterborne navigation will be subject to taxation. Taxes will be calculated according to the net calorific value of the fuel. Tax exemptions will initially incentivize the use of sustainably produced alternative fuels, electricity and shore-side electricity used by vessels at berth. Working from a basis aligned with the established climate goals for 2030, there are three possible ETD variations under discussion:

Option 1 keeps much of the current scope, but includes intra-EU shipping, with transitional exemptions for certain sustainably produced fuels.

Option 2 introduces a system of minimum rates for intra-EU operations – based on energy content – which will increase over a ten-year transitional period. There are two possible variations of this option, one proposing a shorter transitional period, and the other the inclusion of air pollutants in the ETD’s scope.

Option 3 may not apply to the maritime sector, if the maritime sector is included in the EU Emission Trading System.

Points of Concern

The ETD proposal is still subject to change as it remains under discussion at both the EU Parliament and EU Council.* Points raised have included:

The need for a comprehensive assessment of all aspects of the Fit for 55 package

The introduction of a heavy fuels tax for the maritime sector

The clarification that only cleanly produced electricity can qualify for exemption status

The possibility of basing taxation rates on energy content rather than volume

References

EU - Infographic Fit for 55 and ETD

Stories

How much power does a ship actually draw at berth? The same vessel can vary by 300%, sister ships doing exactly the same can differ by 30%, and Tankers of the same size can differ tenfold in installed capacity. This masterclass explains the methodology we use to estimate average shore power demand per ship category, using GT-based scaling functions and calibrated load factors built on 7,102 ships and 153 measured datasets.

Shore power is becoming mandatory in the EU from 2030, but no regulation says what it should cost. This masterclass explains how an OPS connection is defined, the three pricing models used across EU ports, what shipowners currently pay per kWh, and how that compares to generating electricity onboard.

This Q&A looks at how equipment finance and leasing shape decarbonization decisions, with Kevin Swannack and Andy Bailey of Wavefront Asset Management, who explain why and how leasing of equipment can actually be the most cost-effective option.

This case study compares three compliance strategies for FuelEU (paying the penalty (business as usual), buying pool credits from a third party, and blending biofuels) for a representative 4-ship fleet over 2026–2040. Results show that pooling and biofuels both beat business as usual by 6–7%, but it is a coin toss on which is better for you. The outcome is highly sensitive to B100 price and tightens structurally in favour of biofuels after 2030, making this a tipping-point question rather than a one-off choice.

This FAQ provides essential answers on grid balancing markets (FCR, aFRR, mFRR), trading markets (day-ahead, intraday), and congestion management. Covers prequalification timelines, revenue ranges, operator roles, technical requirements, and more. It is intended for developers and asset owners in Northwest Europe.

Batteries can earn money from the grid in three ways: balancing (steady capacity fees), trading (price spreads), and congestion management (local activation). But grid services are fragmented by country, operator, and product: what works in the Netherlands doesn't work in Germany. This guide shows energy storage developers how to stack these three revenue streams for maximum ROI. Intended for developers in port environments.

Every regulator, classification society, broker, and data provider has its own ship-type taxonomy: the same vessel can be a Ro-pax ship to EU MRV, a Cruise Passenger Ship under IMO MARPOL Annex VI, and simply a Passenger ship in a Clarksons fleet report. None of the labels is wrong; they are the working vocabulary of different communities. This blog provides guidance by harmonizing them into the ‘Sustainable Ships framework’: 20 categories, 72 types, and 52 sizes.

Shipping companies face a growing set of regulatory obligations (EU ETS, UK ETS, FuelEU Maritime, and IMO Net-Zero) that directly affect operating costs. This case study determines these costs for a representative fleet of eight Greek dry bulk vessels, calculating exposure under EU ETS, FuelEU Maritime and IMO Net-Zero from 2026 to 2050. The fleet faces a total compliance cost of $4.1 billion over the analysis period, escalating from $30 million in 2026 to $ 362 million in 2050.

This case study determines the cost of generating electricity onboard a ship using auxiliary diesel engines to determine when it is more cost-effective to purchase electricity from the grid in port. Results show that fuel costs alone sit around $0.20 per kWh, but once regulatory compliance costs are layered on top, the total effective costs rise sharply to $1.00 per kWh by 2040.

EMSA and DG MOVE are hosting a dedicated webinar series aimed at supporting maritime stakeholders in navigating the implementation of FuelEU Maritime and its broader regulatory context. The sessions are designed to provide practical insight into how the regulation will be applied in real-world operations, including its impact on fuel choices, compliance strategies, and commercial decision-making across different vessel types and trades.

This case study explores the retrofit of the crude oil shuttle tanker Toril Knutsen to use onshore power supply (OPS) during port stays. The analysis assesses onboard retrofit requirements, power demand at berth, CAPEX, and the resulting business case. Total CAPEX is estimated at around $4M for a conservative tanker-specific configuration. Payback can fall in the range of 1 to 4 years, with most value driven by reduced FuelEU, EU ETS, and IMO-related compliance costs.

Reefers (Refrigerated Containers) increase power demand onboard container ships by approximately 4.38 kW per reefer container. The implication is material: even a relatively small share of reefers can account for a disproportionately large share of total berth power demand. Realtime measurements show that even when 1% of all containers onboard a ship are reefers, it can consume almost 20% of the ship’s total energy demand.

If shore power projects were easy, every port would already have them. Instead, developers run into the same fundamental challenges: unpredictable vessel power demand, complex infrastructure decisions, and business cases full of question marks. In this blog we look at those problems, and how our tools help you tackle them.

AFIR and FuelEU Maritime make the use of onshore power supply (OPS) effectively mandatory but say nothing about what it should cost or how it should be priced. The result is a patchwork of tariff designs and varying levels of transparency, making like-for-like comparisons difficult for shipowners and operators. This blog aims to provide at least some guidance on the matter.

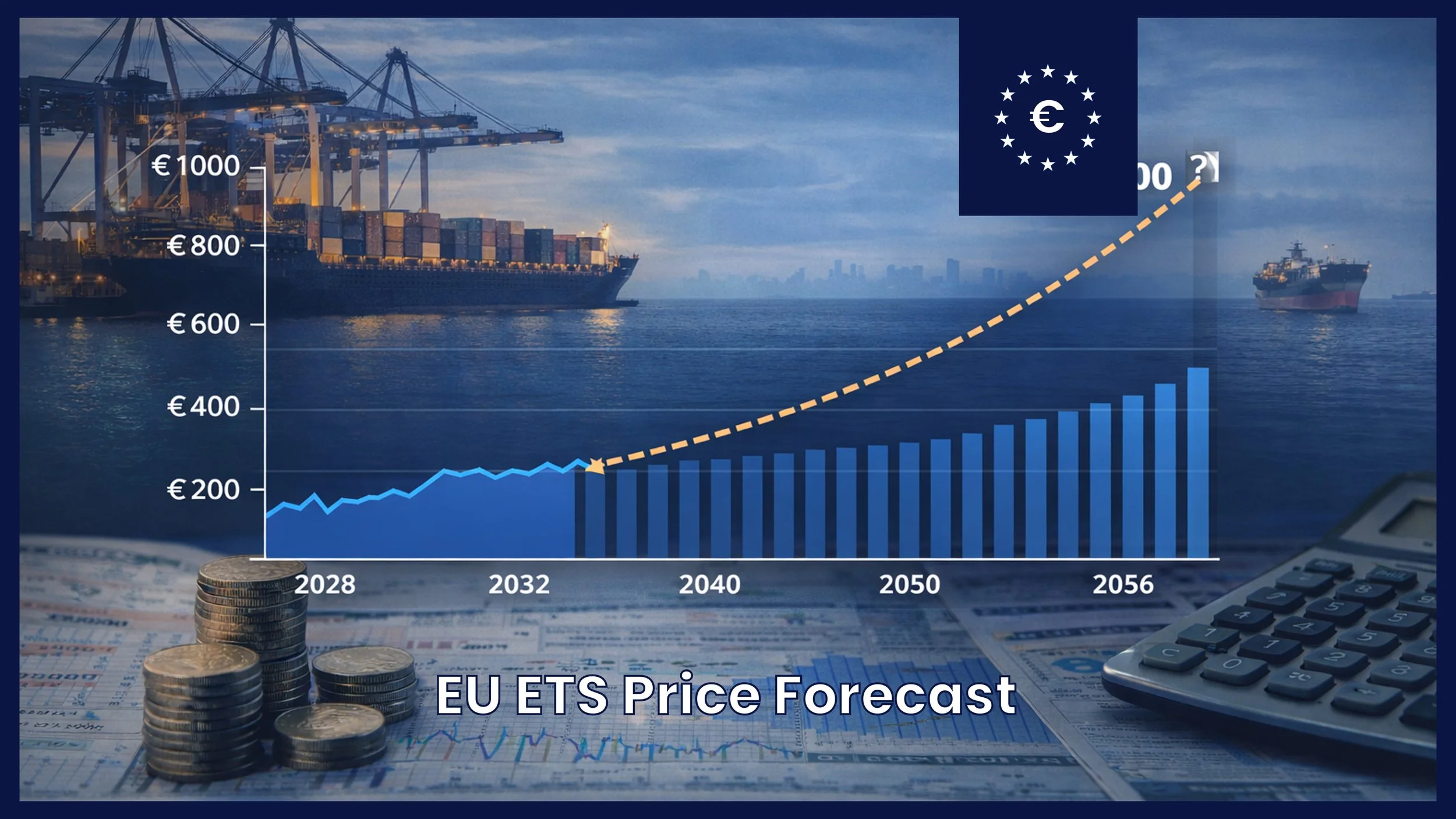

With shipping now included in EU ETS, carbon prices are becoming a major cost driver for maritime transport. As the total amount of emission allowances gradually decreases, prices are expected to rise over time. Many projections assume an increase of roughly 7% per year, potentially reaching €400–€500 per tonne of CO₂ in the long term.

Fuel selection is not only about emissions or cost - tank space often becomes the limiting factor. This article compares marine fuels by volumetric energy density (VLSFO as reference), shows why HFO/LFO have historically dominated, and why methanol is a practical alternative fuel from a ship design perspective. Methanol still requires roughly 2–2.5× the tank volume of conventional fuels, but performs better than ammonia or hydrogen for volume-constrained ships.

This Q&A session explores how transition fuels can support maritime decarbonization today, without major retrofits or new infrastructure. Together with Quadrise, we discussed MSAR® and bioMSAR™, oil-in-water emulsion fuels designed to improve combustion, reduce emissions, and support compliance under EU ETS and FuelEU Maritime. Relevant for shipowners and operators seeking practical solutions for the existing fleet.

When is it more cost-effective to use a B30 or HV30 blend as opposed to regular MDO? This article breaks down the economics of MDO versus biodiesel and HVO blends by comparing VLSFO equivalent costs of fuel over a range of EUA price scenarios. Results indicate that it becomes attractive to use blends at EUA prices above €85.

This Q&A session explores the role of book and claim systems in maritime decarbonization, featuring Himanshu Sharma from Vurdhaan, a platform providing independent registries for Scope 3 emission reductions. Himanshu explains how virtual crediting works, why transparency and verification are key, and how book and claim differs from compliance pooling under FuelEU Maritime.

When does the use of shore power become cost-effective for shipowners under new EU and IMO regulations? Using the Shore Power Quickscan, this article breaks down key cost components such as fuel, electricity, EU ETS, FuelEU Maritime, and the upcoming IMO Net-Zero framework and compares cost impact of different routes on a 2,500 TEU containership. Results show that while shore power can already deliver savings from 2025 onwards (!), its competitiveness strengthens sharply after 2030 as compliance costs rise.

Shipowners and operators face the challenge of navigating multiple regulatory frameworks - EU ETS, FuelEU Maritime, and IMO Net-Zero - each employing distinct methodologies and emission factors for assessing fuel emissions. This blog provides clear guidance on the differing emission factors and calculation methods employed by each regulatory framework.

Accurate assessment of marine fuel costs is becoming increasingly critical as regulatory pressure grows, especially given the recently announced IMO Net-Zero Framework. This blog uses a VLSFO-equivalent cost model to evaluate the impact of FuelEU Maritime, EU ETS, and IMO Net-Zero regulations on a wide range of fuels. By comparing fossil, bio-based, and synthetic fuels under realistic scenarios, the analysis shows that compliance costs - driven by emissions penalties and carbon pricing - are expected to exceed fuel prices by 2030 for many options.

This Q&A session explores the upcoming IMO Net-Zero Framework, featuring Rajat Bishnoi and Yuvraj Thakur from Normec Verifavia, an accredited verifier supporting shipowners with emissions reporting and regulatory compliance. They explain the new GHG Fuel Intensity and Fuel Standard requirements, compare them to FuelEU Maritime, and discuss penalties, registry systems, and practical implications for shipowners preparing for 2027–2028 enforcement.

Accurate estimation of shore power demand at EU ports has become essential due to strict regulations like AFIR, which requires electrification for 90% of port calls by container and passenger ships at TEN-T ports by 2030. This blog evaluates three methods—using EU MRV fuel data, Sustainable Ships’ ship-specific power database, and ICCT research—to estimate the Total Addressable Market (TAM) for shore power. Results show the total annual electricity demand across EU ports is between approximately 6 and 13 TWh, highlighting the significant scale of infrastructure investment ahead.

This case study explores a 100 kWp solar PV system installed on the hatch covers of a handymax bulk carrier. Operating primarily in Northern Europe, the system offsets auxiliary engine load during idle periods, leading to estimated savings of ~$350,000 between 2025 and 2035. With a CAPEX of $100,000, the payback period is around three years. Most savings come from fuel reduction, with additional benefits from EU ETS and FuelEU compliance. The business case is most sensitive to engine efficiency (SFC) and fuel price.

This case study evaluates a mobile shore power battery barge designed for an offshore construction vessel in the Port of Rotterdam. An average power demand of 2.4 MW and a peak demand of 5 MW is assumed. This results in the requirement of twelve 20-ft containerized batteries integrated into a High Voltage Shore Connection (HVSC) system. Total costs of the power barge are estimated at $9.5M with a yearly revenue of approx. $2.5M.

This Q&A session explores the role of biofuels in decarbonizing maritime transport, featuring Johannes Schurmann, Commercial Director Marine at FincoEnergies, supplier of biofuels and supporting shipowners in adopting biofuels with end-to-end services, from technical assessment to regulatory documentation. Johannes shares insights into market developments, pricing trends, regulatory impacts, and operational considerations, focusing on the practicalities of switching to biofuels.

This Q&A session explores the role of low-carbon ammonia in decarbonizing the maritime industry, featuring Jean and Paul, co-founders of Ten08, a Houston-based company developing low-carbon ammonia for industrial and maritime use. Ten08’s mission is to supply the maritime sector with scalable and clean ammonia.

Operating an offshore workboat in the North Sea area until 2050 will impose significant financial and operational pressure due to tightening environmental regulations and mounting compliance obligations. Modelling of compliance costs shows a clear tipping point in 2040, with FuelEU Maritime becoming the dominant driver, although FuelEU currently applies to vessels above 5,000 GT only. Results for a large offshore workboat operating year-round in the North Sea show that the maximum projected cost exposure could reach up to $250 million between now and 2050.

Choosing a marine fuel is no longer about price per metric ton, it is about total regulatory exposure. This masterclass covers 22 marine fuels across three groups and six families, how EU ETS, FuelEU Maritime and IMO Net-Zero each calculate costs differently, and why 2035 is the tipping point that should drive your decision.